For more stories like this, sign up for the PLANSPONSOR NEWSDash daily newsletter.

Opinions June 6, 2025

Addressing the “Alternative Investment Gap” in DC Plans

A strategist for PGIM DC Solutions reviews how including alternatives among defined contribution plan investments can affect retirement outcomes, and what to consider.

Reported by Jeremy Stempien

Jeremy Stempien

In our latest DC landscape survey, we explored defined contribution plan decisionmaker perspectives across a variety of domains. We found that overall satisfaction with respect to plan investments was relatively high, especially in areas such as asset class diversification, overall performance and cost.

One area in which there appears to be a disconnect is alternative investments. Despite clear interest from DC plan decisionmakers, alternative investments are not commonly featured today in core menus, nor are they widely used in professionally managed portfolios such as target-date funds. Our research indicated that including a more extended list of investments can improve expected returns, which can create better potential retirement outcomes for DC participants.

Therefore, increasing the availability and usage of alternative investments in DC plans is something that should continue to be a key focus for plan sponsors and DC consultants.

The Evolving DC Landscape

Our latest plan sponsor survey was conducted by Greenwald Research and included 302 retirement plan decisionmakers, who were surveyed online in September and October 2024. Respondents included decisionmakers for DC plans with at least $10 million in plan assets. Findings were weighted by plan asset size, using data from a BrightScope/ICI 2021 report.

In our survey, we found that plan sponsors had relatively positive views on alternatives. For example, 73% agreed that TDFs should include allocations to alternative investments, such as real estate or commodities, to enhance diversification.

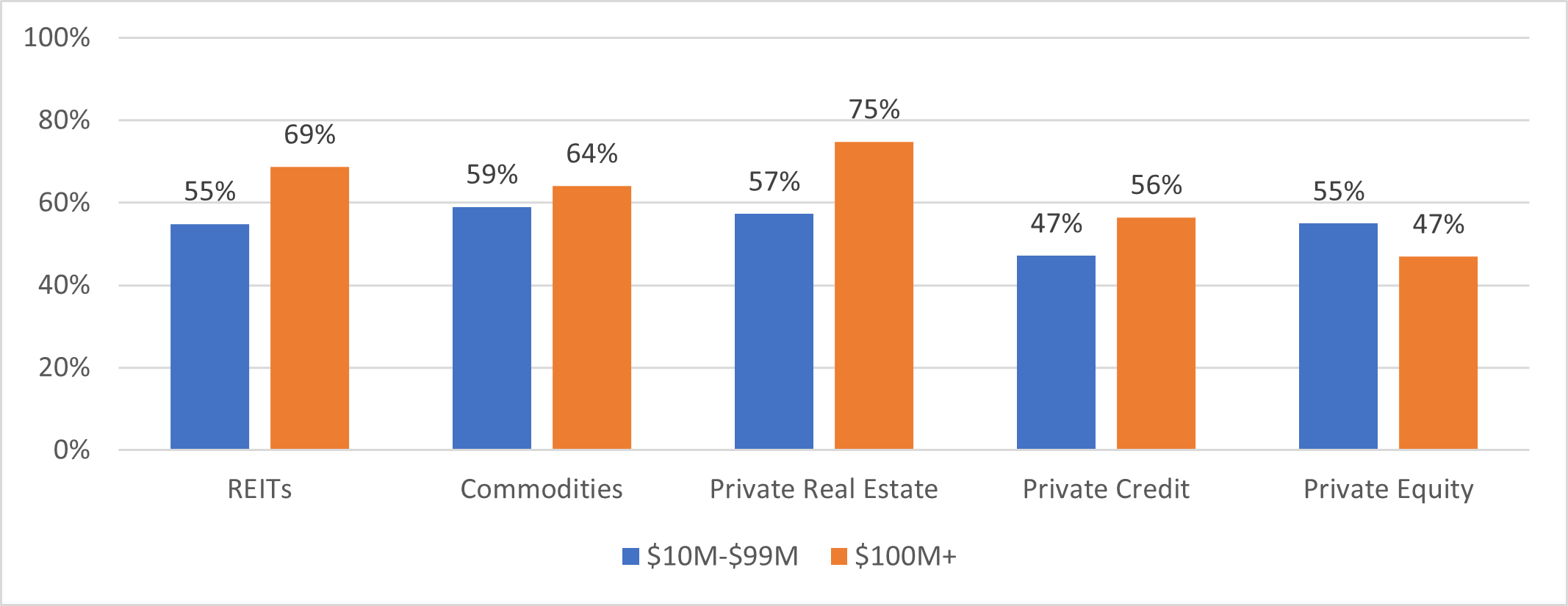

We also asked about the inclusion of certain individual asset classes should in target-date funds, with a goal of improving long-term performance. We have broken out the responses into two groups based on plan size: plans with between $10 million and $100 million; and those with at least $100 million in assets. There were clear differences between the two groups’ responses, included below.

Should Target-Date Funds Include the Following Alternative Investments to Improve Long-term Performance

Source: 2025 PGIM DC Landscape Report

The chart indicates that interest in alternatives is relatively high, especially among larger DC plans. While it isn’t clear what the source of this higher conviction among larger plan sponsors is, it could be familiarity with the investments in other areas, such as defined benefit plans.

Among the three private asset classes included (private real estate, private credit and private equity), interest in private real estate was clearly the highest. Looking deeper into the private asset classes, additional responses suggested that fiduciary risk is a key concern, as only about half of DC plan decisionmakers thought the long-term performance of the asset class protected it from fiduciary risk. The private markets are still developing, and while we expect some DC plan sponsors to remain cautious, we think concerns will likely decline as acceptance and utilization increase across plans.

The clear interest in alternative investments is in somewhat stark contrast to their general availability in DC plans today. For example, our recent piece suggested that real estate funds are available in less than 40% of 401(k) plans, and commodities funds are available in less than 5% of plans. These asset classes also tend to have relatively small weights to TDFs as well.

We believe one reason that alternatives are featured more heavily in professionally managed portfolios is that the risk of private investments often is not accurately captured. We covered this in a recent research piece for the CFA Institute, in which we demonstrated how the risk of commodities changed dramatically when explicitly considering inflation as part of the portfolio optimization routine and focusing on longer investment horizons (since returns are not completely random across time).

Additionally, we have found that extending the portfolio opportunity set beyond a relatively basic set of asset classes can potentially improve risk-adjusted performance by approximately 100 basis points, which could result in five or more years of income in retirement. In other words, a well-constructed portfolio that includes alternatives has the potential to significantly improve retirement outcome for DC participants.

Conclusions

While alternative investments are common in DB plans, they are still relatively rare in DC plans. Our latest DC landscape survey suggested that a potential gap exists, whereby plan sponsors are becoming interested in alternative investments to improve diversification and portfolio returns, but availability is relatively limited. Therefore, while we do see evidence that plan sponsors are relatively content with their investments today, there still remains room for improvement.

Jeremy Stempien is a managing director, portfolio manager and strategist for PGIM DC Solutions, the retirement solutions provider of PGIM, the principal asset management business of Prudential Financial.

This feature is to provide general information only, does not constitute legal or tax advice, and cannot be used or substituted for legal or tax advice. Any opinions of the author do not necessarily reflect the stance of ISS STOXX or its affiliates.