Get more! Sign up for PLANSPONSOR newsletters.

Opinions May 19, 2025

Dementia’s Financial Toll: How Losses Can Often Predate the Diagnosis

Experts from the MIT AgeLab explore the financial costs of dementia and how they manifest.

Reported by

Joseph Coughlin and Luke Yoquinto

Art by Shout

Editor’s note: The name of the caregiver in this article, Angela, was changed to protect her privacy and her family’s.

When Angela looks back at the financial costs imposed by her mother’s dementia, the expenses that spring to mind most readily are the ones that came after the diagnosis. That was when Angela and her family began paying for experimental treatments out of pocket while undergoing a grueling travel schedule.

“There were so many appointments, questions, practitioners,” she recalls. Then there was the in-home care. “The costs are extraordinary.”

When many of us think about the financial implications of Alzheimer’s disease and other forms of dementia, these types of costs, arriving in the wake of a diagnosis, may be the first to spring to mind. A recent research effort, however, is uncovering a concerning new layer to dementia’s financial toll: the money lost before the diagnosis.

In the years leading up to a dementia diagnosis, individuals’ cognitive capacities begin to change, subtly at first, while they maintain full control of their finances. At the same time, they or their family members may find it necessary to dial back their working hours: to provide care or because work has become too difficult. Profound vulnerability to financial losses is the result. In most cases, money will have begun leaking out of the accounts of those affected six to eight years before their cognitive issues become impossible to ignore, when they or their families consult a physician.

Pre-Diagnosis Losses

In the case of Angela’s mother, the financial impacts began several years before the family knew with certainty they were dealing with dementia. There were “definite costs before the diagnosis,” Angela says. Physical health issues, which turned out to be linked to the dementia, were the first hint something was wrong. To cope with them, the family commenced an expensive series of home modifications. Meanwhile, to better provide care, Angela’s father entered semi, and then full, retirement—another cost, in the form of lost income.

Angela’s family’s experience is in no way unique: Pre-diagnosis financial losses are exceedingly common when it comes to dementia. What is less clear, however, is what is causing these losses and whether the specifics in Angela’s case—reduced income, new expenses—represent what’s happening in the population at large.

Equally thorny is the question of a remedy. What, exactly, can financial and medical professionals, among the many others who might get involved, do to stem the tide of financial losses?

Today, researchers across the U.S. are shedding light on this still-mysterious period: working backward to compare the pre-diagnosis finances of individuals who ultimately developed dementia against those lucky enough not to. This line of work, part of a surge in dementia studies that took off in 2012 thanks to a major, federal investment in Alzheimer’s research, bore fruit in 2021. That year, a study of Medicare recipients revealed that for individuals living alone who went on to be diagnosed with dementia, indications of financial trouble began as early as six years beforehand, taking the form of missed payments and declining credit scores.

A 2023 study expanded on this work: assessing the pre-dementia period’s impacts not just on payments and credit reports, but on overall wealth, and not just for individuals, but for the entire households of people with dementia.

The results were stark. In the eight years leading up to a dementia diagnosis, the median U.S. household net worth drops to less than half that of households without dementia: $104,000, compared with $217,000.

These findings raised eyebrows—including some at AARP.

“We were surprised to learn how much wealth people can lose leading up to a formal dementia diagnosis,” says Julie Miller, the organization’s director of thought leadership for financial resilience.

Any successful remedy would likely involve actors across dizzyingly disparate fields, ranging from general and specialized medicine to the legal field to financial planning, spanning business, nonprofit and government sectors.

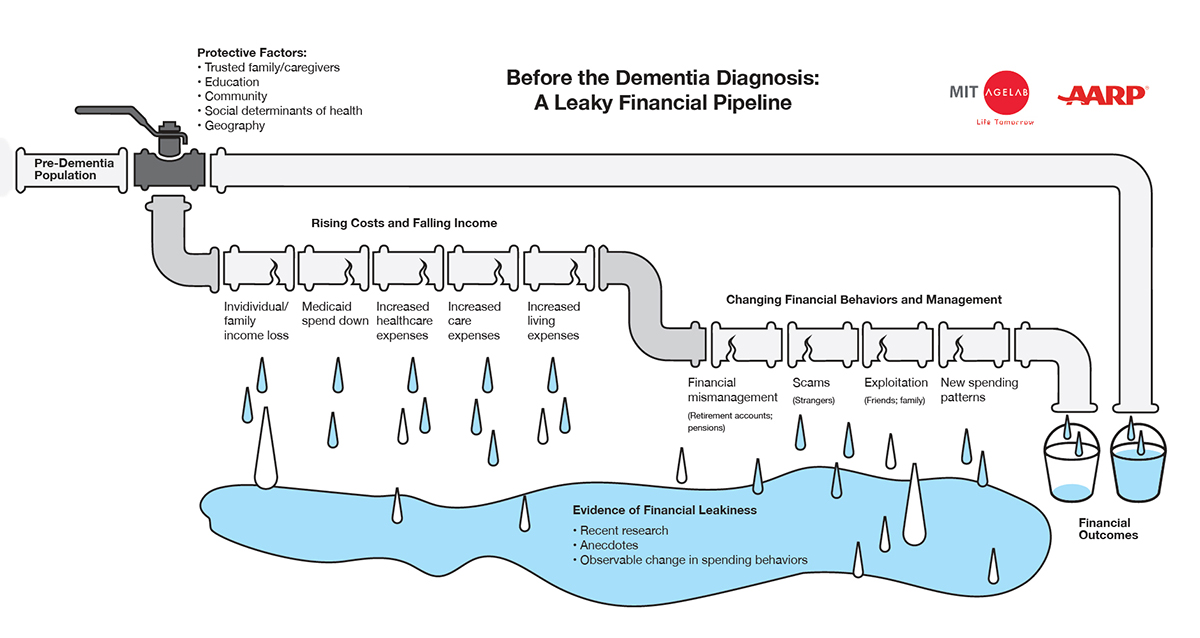

Cracks in the Pipeline

To make the issue more tractable, AARP brought in our organization, the Massachusetts Institute of Technology AgeLab. We produced a visual metaphor to illustrate the mystery of the disappearing pre-dementia funds, analogizing an individual’s pre-dementia finances to a leaky pipe. Compared to the watertight pipeline representing those lucky enough to avoid dementia, the pre-diagnosis pipeline contained a number of cracks: potential sources of financial losses, dripping onto the floor.

These belonged to two categories. The first consisted of costs that, though unfortunate, were hard to prevent: care and medical expenses, for instance, or reduced income due to someone stepping back at work. Then there were costs in the more preventable category: losses created or enabled by cognitive changes, including financial mismanagement; new, harmful spending patterns; and increased susceptibility to scams and fraud.

All these explanations were on the table when the MIT AgeLab and AARP convened a conference at MIT in April 2024. Different industries, we argued then and in the ensuing report, had different roles to play. More doctors ready to diagnose dementia were needed. Lawyers, too, could help in many cases, but not all. Unfortunately, people with undiagnosed cognitive impairments are unlikely to have protective legal measures in place, such as a proxy, leaving them exposed to scams and fraud.

Potential Warning Signs

The financial advisory field may prove an especially important part of the solution. Because financial missteps, such as missed payments, can serve as a warning sign of cognitive impairment, advisory professionals may be well positioned to notice when something’s wrong.

For retirement plan sponsors and fiduciaries, these early financial missteps—including irregular contributions, hardship withdrawals or sudden shifts in investment behavior—may serve as subtle red flags. By integrating plan data monitoring with educational outreach or even soft-touch, wellness interventions, employers could potentially help identify and support at-risk employees and families before a formal diagnosis is made or before major financial harm occurs.

Individual and family financial advisers, meanwhile, upon noticing something amiss in a client’s finances, may recommend consulting a doctor. That is not always an easy topic to broach, however. Often, says Josh Rundle, head of retirement solutions at Transamerica, these conversations require having multiple family members, even multiple generations, in the room.

“There is a stigma attached to cognitive decline—it’s progressive, there is no cure, and that makes some feel helpless,” he says. Financial advisers must “invest in their soft skills and begin to normalize these planning conversations with their clients and their loved ones, ideally before a diagnosis.”

Taking on these conversations, he says, though challenging, can give a family a sense of “understanding, preparedness and peace of mind.”

More Research to Come

Continued research into the mysterious drivers of financial losses, meanwhile, places still greater emphasis on steady financial advice. With a team of collaborators, the University of Washington health economist Jing Li, lead author of the 2023 paper on household wealth, is drilling down into possible causes.

New results not yet published, she says, suggest that investment accounts, as opposed to checking or savings accounts in which people park cash, take the biggest losses in the pre-diagnosis period. That means new spending habits may not be driving the bulk of the financial losses.

“A conjecture,” she says, “is that financial mismanagement could be responsible for some of these losses”—for instance, when someone panics and sells their assets at the bottom of a downturn. A steady advisory hand may help households avoid such outcomes.

Obtaining an earlier diagnosis, too, corresponds with reduced wealth losses, although Li says more research is required to identify what, if anything, is acting as the protective factor.

“Maybe people who get an early diagnosis are also likely to have family members watching them more closely,” she says.

Wealth losses in the leadup to a dementia diagnosis were not unheard of prior to the recent flowering of research into this topic, but they tended to be the subject of anecdote and viewed mainly as a warning sign for diseases like Alzheimer’s. Increasingly, however, researchers and practitioners are treating such losses not just as an indication of possible dementia, but among its major harms.

Continued research into these losses, as well as a growing sense of urgency among doctors, lawyers, regulators and advisers, may make this issue less mysterious—and less financially devastating.

Joseph Coughlin is director of the Massachusetts Institute of Technology AgeLab. He is the author of “The Longevity Economy: Unlocking the World’s Fastest-Growing, Most Misunderstood Market” (Public Affairs, 2017).

Joseph Coughlin is director of the Massachusetts Institute of Technology AgeLab. He is the author of “The Longevity Economy: Unlocking the World’s Fastest-Growing, Most Misunderstood Market” (Public Affairs, 2017).

Luke Yoquinto is a researcher at the MIT AgeLab. He is the coauthor of “Grasp: The Science Transforming How We Learn” (Doubleday, 2020).

Luke Yoquinto is a researcher at the MIT AgeLab. He is the coauthor of “Grasp: The Science Transforming How We Learn” (Doubleday, 2020).

Together, Coughlin and Yoquinto are editors of “Longevity Hubs: Regional Innovation for Global Aging” (MIT Press, 2024).

This feature is to provide general information only, does not constitute legal or tax advice, and cannot be used or substituted for legal or tax advice. Any opinions of the author do not necessarily reflect the stance of PLANSPONSOR, ISS Stoxx or its affiliates.

« Cigna Hit With Forfeiture Lawsuit; Intuit Reaches Settlement