For more stories like this, sign up for the PLANSPONSOR NEWSDash daily newsletter.

Opinions September 22, 2021

HSA Investment Options and Best Practices

Peg Knox, with DCIIA, presents data and recommendations for health savings account investment lineups.

A health savings account (HSA) is a powerful tool for saving and paying for health care expenses.

HSAs are available only in combination with a high-deductible health plan (HDHP) and are designed to allow individuals to save for current and future medical expenses on a tax-efficient basis. A recent PLANSPONSOR article touched on the many features and benefits of HSAs, including the fact that “contributions are tax-free, profits on investments are tax-free and withdrawals used for qualified medical expenses are tax-free.”

According to HSA investment adviser and consultant Devenir, “One way that institutions can help account holders take full advantage of their HSAs is to offer investments. Adding investments allows account holders to potentially maximize their tax savings, earn more on their unused dollars and potentially build a larger nest egg for health care expenses in retirement.”

Most HSAs currently require a minimum balance in the account before participants can invest assets. In its “2020 Health Savings Account Landscape” report, Morningstar cautions against this requirement, noting that accountholders should be able to invest without meeting a minimum balance threshold, as this creates an opportunity cost, especially in the current near-zero rate environment.

In a 2020 white paper, DCIIA noted that once investments are added, “HSAs then become more than just a checking account for medical expenses; they are part of a comprehensive retirement savings and investment strategy. … Employers should evaluate a range of HSA providers by conducting a thorough review of current HSA offerings in the marketplace. HSA platforms have changed over the past several years, with many now offering features similar to those found in defined contribution (DC) plans.”

Examining Investment Options

In its “2021 HSA Survey,” the Plan Sponsor Council of America (PSCA) notes that 84% of organizations surveyed offer investment options for HSA contributions, and, of those, 95% indicated that their HSA provider determined the investment options. In terms of types of investments offered, 94% offer mutual funds, 28% offer a self-directed brokerage (SDBA), 8% offer certificates of deposit (CDs) and 10% offer exchange-traded funds (ETFs).

A plan sponsor can select an HSA provider that offers investment options that replicate those in their 401(k)/403(b) plan. This type of “mirroring” can simplify the employees’ investment decisionmaking process by reducing the choices they face when selecting where to invest their savings. However, PLANSPONSOR’s 2021 Health Savings Account Survey found only 1.9% of organizations exactly mirror their offerings and 17.5% indicated that the HSA investment lineup overlaps but does not mirror their DC plan investment lineup.

Callan reported in its most recent annual “DC Survey” that the benefits committee oversaw the HSA program for six in 10 survey respondents. Only 17% of sponsors selected the HSA provider and undertook the additional responsibility of selecting and monitoring underlying investments.

Regardless, employers should understand their HSA investment lineup and the HSA provider’s process in determining which funds are offered. They should also be aware that HSAs are not governed by the Employee Retirement Income Security Act (ERISA), and DC plan assets cannot be commingled with those of the HSA in the same investment fund.

When considering HSA investments, some questions employers may ask include:

- Does this lineup make sense?

- Do options include target-date funds (TDFs) or balanced funds?

- Are the investment strategies robust offerings for my employees?

- Are the investment fees reasonable?

- Is there any flexibility to the provider’s “standard lineup”?

Morningstar suggests best practices for HSAs offering investment options, including:

- Offering investment strategies in all core asset classes while limiting overlap among options;

- Providing strong investment strategies; and

- Charging low fees for both active and passive strategies.

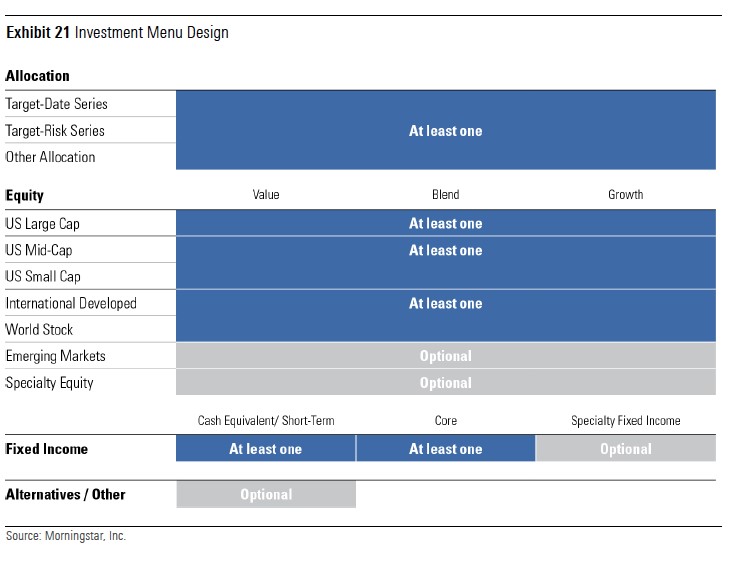

It also notes, “We believe the ideal number of investment offerings is around 12 to 24, with a bias toward the lower end of that range.” The exhibit below, from its “2020 Health Savings Account Landscape” report offers more detail about its suggestions.

Devenir research indicates that there are now approximately 1.7 million accounts in which participants are investing a portion of their HSA dollars, representing almost 6% of all accounts and 29% of all HSA assets. It also reports a $17,926 average total balance (deposits and investments combined) for HSA investment accounts, noting this is “6.5 times larger than an average funded non-investment holder’s account balance”—supporting the notion that access to and use of investments could have a substantial impact on a participant’s overall savings.

Focusing employee education on the long-term impact of saving in an HSA, both from an investing and tax perspective, can help employees understand how to get the most from their HSAs and encourage them, when possible, to make the HSA a key element of their overall retirement strategy.

Peg Knox is the chief operating officer (COO) of the Defined Contribution Institutional Investment Association (DCIIA) and is a former plan sponsor.

For more information about HSAs, see PLANSPONSOR’s article, “What Employers Need to Know About HSAs,” and DCIIA’s “The HSA: The ‘S’ is for Savings (not Spending!)” white papers (Part I and Part II).

This feature is to provide general information only, does not constitute legal or tax advice and cannot be used or substituted for legal or tax advice. Any opinions of the author do not necessarily reflect the stance of Institutional Shareholder Services Inc. (ISS) or its affiliates.