For more stories like this, sign up for the PLANSPONSOR NEWSDash daily newsletter.

Opinions July 15, 2019

Volatility and TDFs: The Good, the Bad and the Unintended

John Greves, Natallia Yazhova and Jake Gilliam, with Charles Schwab, discuss volatility as it relates to target-date funds (TDFs) and how plan sponsors may want to re-examine risk exposures in these vehicles.

One of the appeals of multi-asset-class portfolios such as target-date funds (TDFs) is their potential to provide retirement plan participants with a smoother ride when markets are volatile. It’s important to remember, though, that volatility cuts two ways, and that can be hard to see when U.S. equity markets have been rising steadily for more than a decade.

Exposure to volatility is not necessarily a bad thing. Volatility is simply a measure of the range of price changes—both up and down—an investment experiences over a period of time. The more stable the price, the lower the relative volatility, and vice versa. Considered as such, volatility is a measure of investment risk, because higher levels imply that a portfolio’s returns may be less predictable, yet taking that risk can enable the return necessary for long-term wealth accumulation.

Now let’s apply that to what we’ve seen in the markets. Over the 10-year period from March 2009 to March 2019, the Standard &Poor’s (S&P) 500 Index generated an impressive 17.5% annualized total return, assuming reinvested dividends. That’s well above the benchmark’s average annualized total return of 9.4% over the past 90 years.

This highlights the benefits of “upside” volatility.

Of course, while nobody knows exactly when the bull run will end, it’s fair to assume it won’t go on forever. So it’s important to be aware of, and ready for, potential “downside” volatility.

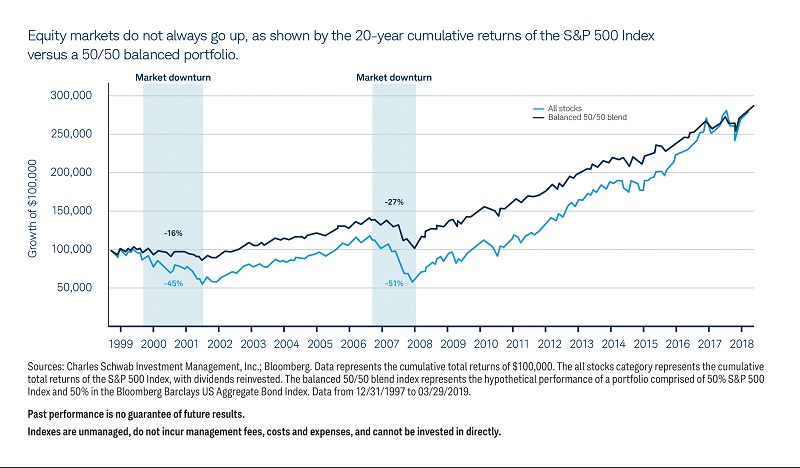

Over the past 20 years, there have been two major market declines where the S&P 500 Index lost 45% or more of its value. Such an event could prove to be a devastating loss for retirement investors overexposed to equities and unlucky enough to have to redeem assets during the months when the index was falling or during the subsequent years it took to recover. Portfolios that include more diversified exposures can help protect assets during such downturns, providing a smoother long-term investment path.

Additionally, TDFs automatically rebalance without requiring investors to take action, providing another level of protection against volatility regardless of the direction the market takes.

Check risk exposures

Many multi-asset class portfolios and TDFs have been riding a wave of upside volatility for so long that this can mask their potential downside risk in less favorable markets. This can conceal unintended volatility—too much downside risk and potential loss exposure relative to a participant’s tolerance and/or goals—in two pivotal ways:

- Downside volatility exposure may be masked by extended upside outperformance. More aggressive portfolios with greater volatility exposures have generally outperformed more conservative allocations over the past three-, five- and 10-year periods. These gains fail to indicate how volatile these portfolios may be on the downside should markets begin to experience less constructive investment climates for extended periods.

- Additional volatility exposure may have crept into the portfolio. As markets move higher, the degree of potential downside volatility exposure in a portfolio can increase as well, which can introduce inappropriate amounts of volatility. Inadequate portfolio rebalancing can distort risk levels, as allocations that are more volatile grow in proportion during rising markets.

As a result, it is critical for plan sponsors and their advisers to re-examine risk exposures as part of their regular review of target-date funds.

Volatility, time horizons and cash flows

Two critical considerations for portfolio volatility exposures within a TDF are time horizon and cash flows. Time horizon is crucial to evaluate because the shorter the horizon, the higher the potential risk of distortion from market volatility. Cash flows into or out of a portfolio directly influence the dollar-weighted return that is generated over time as markets fluctuate.

Generally, TDF investors just starting their career with long time horizons and limited savings can benefit from significant volatility exposure, as this can help them accumulate wealth over time and benefit from the ups and downs of the market through dollar cost averaging.

As investors accumulate wealth and approach and enter retirement, however, higher levels of volatility can work against them in a number of ways.

First, it can cause them significant stress when balances fluctuate, given the larger dollar impact and generally shorter recovery times before investors need to tap into assets.

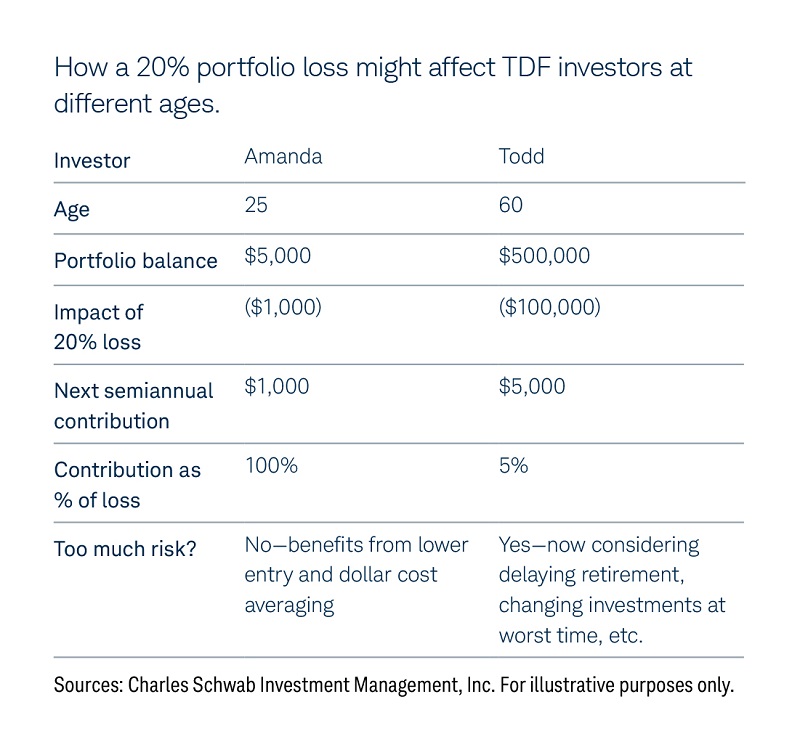

Consider how a hypothetical 20% portfolio loss might affect two TDF investors, one at age 25 and one at age 60.

The younger investor, Amanda, has recently started to invest $1,000 on a semiannual basis and has only saved $5,000, while the older investor, Todd, has accumulated $500,000 and is contributing $5,000 semiannually.

Although both of their portfolios fall by the same percentage, Amanda experiences a much smaller dollar loss—-$1,000 vs. -$100,000—given her much smaller portfolio balance. Her $1,000 semiannual contributions, while well below Todd’s contributions of $5,000, are also proportionately much larger relative to her dollar loss and remaining portfolio balance. Hence, she is able to recover her full original balance with one contribution, investing at lower security prices and with a 30-year-plus time horizon for markets to recover before needing to access assets.

In contrast, Todd has lost tremendous wealth that will likely take much longer to recoup, if ever. As he moves into retirement, he also will no longer be able to benefit from dollar cost averaging when the market falls. Indeed, the opposite is usually the case, as this is when withdrawals tend to begin, and the negative one-two punch of selling assets as values are declining can be devastating to a portfolio.

Unfortunately, too many TDF glide paths keep equity allocations at higher levels near and into retirement, justifying the higher risk exposures with a need to help support a multi-decade spending horizon. Yet, this approach risks exposing investors to too much unintended volatility at the absolute worst time.

Further, industry research has consistently shown that many investors are saving too little for retirement. Many TDF managers often argue that relatively higher equity allocations are necessary at all life stages to help solve for this potential shortfall, in essence trying to offset poor savings behavior by doubling down on equity markets. In our view, this is similar to going to a casino with your last $20 hoping to generate next month’s rent—a very risky gamble that may potentially derail retirement savings. The reality is that no TDF design or amount of equity exposure can offset decades of poor savings behavior.

Conclusions

Given how much and how long U.S. equity markets have risen over the past decade, plan sponsors and their advisers may want to review and critically examine the potential risk exposures currently embedded in their TDF portfolios. Years of mostly upside volatility have been incredibly additive for many multi-asset-class portfolios, but this may have also paved the way for increased levels of unintended volatility on the downside.

To help evaluate portfolios, plan sponsors and their advisers should:

- Recognize that upside volatility and downside potential tend to be closely linked—the strongest investment performers in upmarkets may fall the most in down-markets.

- Be mindful of this volatility and make deliberate decisions for the workplace retirement plan as to appropriate exposure levels based on risk tolerance, time horizon and investment objective.

- Look beyond past investment performance, as a rising equity tide can lift all riskier portfolios.

Above all, be prepared for the reality of volatility. A well-structured multi-asset-class portfolio that matches expected risk to goals and behaviors across a broad range of possible market scenarios can reduce the risk of unintended volatility, offering a more positive overall investment experience and helping to optimize potential performance outcomes over full market cycles.

John Greves is head of multi-asset strategies and Natallia Yazhova is a senior research analyst, both with Charles Schwab Investment Management, Inc. Jake Gilliam is head client portfolio strategist, multi-asset strategies, with Charles Schwab & Co., Inc.

This feature is to provide general information only, does not constitute legal or tax advice, and cannot be used or substituted for legal or tax advice. Any opinions of the author do not necessarily reflect the stance of Institutional Shareholder Services (ISS) or its affiliates.

Charles Schwab Investment Management, Inc., is an affiliate of Charles Schwab & Co., Inc., and a subsidiary of The Charles Schwab Corporation.

« Plan Sponsor Investment Considerations for Second Half of 2019