Never miss a story — sign up for PLANSPONSOR newsletters to keep up on the latest retirement plan benefits news.

Benefits October 8, 2025

Middle Class Financial Resilience Remains Greater Than Historical Norms, but Pressure Mounts

Both inflation and softening income growth may threaten middle income households’ financial well-being.

Reported by Emily Boyle

Middle class households remained financially resilient in the second quarter of 2025, but they face mounting pressure, according to the American Council of Life Insurers’ October 2025 Financial Resilience Index.

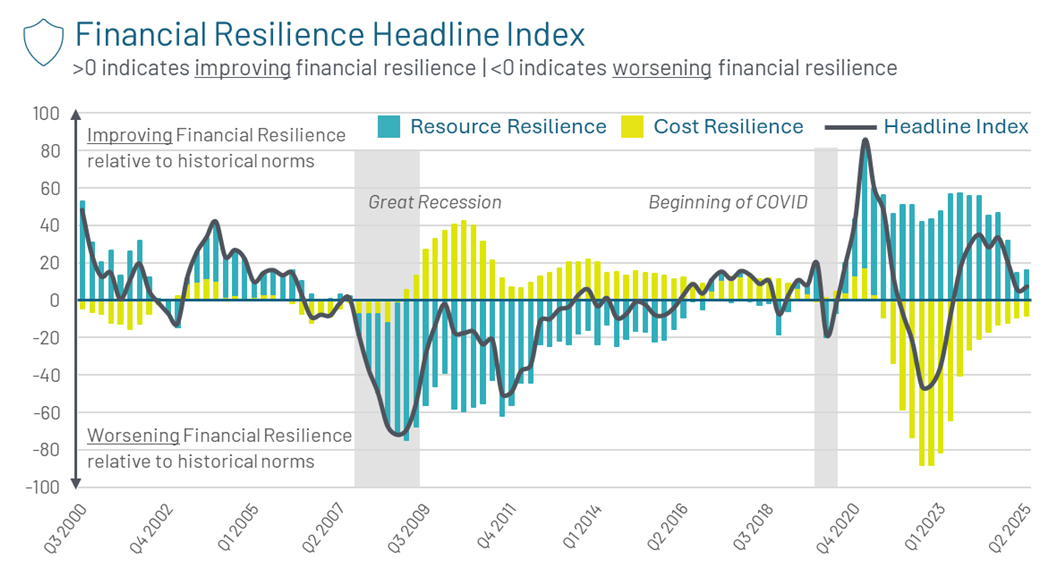

Source: October 2025 Financial Resilience Index, American Council of Life Insurers

According to ACLI data, the headline index—the score used to measure households’ overall financial resilience—was 7.3, up two points from the previous quarter. Scores greater than “0” indicate improvement, while scores lower than “0” show resilience is getting worse. The index remained in positive territory for the eighth consecutive month—but is down 21 points from Q2 2024.

Continued inflationary pressures that are greater than historical norms and slowing income growth may be driving concerns for middle class households, according to a companion survey released with the index. Key findings showed that many middle class households are nervous about the future, with 50% concerned about their ability to afford daily essentials over the next year, up from 38% at this time last year. In addition, 41% of middle class households surveyed said they would go into credit card debt or borrow via a personal or family loan to pay for an unexpected $5,000 expense.

“While the stability of the financial resilience index is a positive sign for people’s overall economic well-being, many middle-class families still struggle with unexpected expenses,” said ACLI President and CEO David Chavern in a statement. “The guidance, products and tools life insurers offer protect Americans from these and other challenges to their financial futures.”

The resource resilience index, which measures the ability to handle unexpected expenses and sustain a quality of life, rose slightly in Q2, with improvements in “access to capital” (a 4.2-point increase from Q1) and “retirement readiness” (a 3.1-point uptick), offsetting a 6.1-point decrease in “income” growth. Asset values for defined contribution plans and life insurance annuities bounced back in Q2 after dipping in Q1, spurring the quarter-over-quarter increase in retirement readiness.

The cost resilience index, which measures the ability to afford modern luxuries, likewise shifted minimally—but trended upward for the 10th consecutive quarter. A slight easing in cost pressures for “essentials” (increasing the index by 2.8 points) offset an increase in inflation for “modest luxuries” (decreasing the index by 2.5 points), while inflation for “care and education” was slightly down from the historical average.

The cost pressure of children’s day care has been greater than average for the past three years, but the inflation of childcare prices has slowed in recent quarters, according to the research. More middle class families with children younger than 18 said they are concerned about their ability to sustainably afford housing over the next year (42%) than did other middle class households (36%).

Meanwhile, including August, foreclosure filings have been up, year-over-year, for six consecutive months and were up 18% from the same period in 2024, according to property data firm ATTOM. Through June, roughly 188,000 properties had foreclosure filings, putting the U.S. on track to surpass the roughly 322,000 U.S. properties that went into foreclosure in 2024.

ACLI’s Financial Resilience Survey is released quarterly. The latest survey was conducted online by YouGov on behalf of ACLI from September 12 to 16, among 3,330 adults aged at least 18. The survey included 1,249 respondents from middle class households, defined as those earning between $50,000 and $149,999 in annual household income.

« Litigation Risk Thwarts Plan Sponsor Innovation, per American Benefits Council