Never miss a story — sign up for PLANSPONSOR newsletters to keep up on the latest retirement plan benefits news.

Opinions February 26, 2020

Now Is the Time: The Retirement Tier

Peg Knox, Defined Contribution Institutional Investment Association (DCIIA) discusses the “retirement tier,” which allows a DC plan sponsor to broaden the plan’s goal from accumulation to decumulation.

If you’ve heard the term “retirement tier” recently and haven’t paid much attention to it, as a former plan sponsor, I urge you to do so. For the first time since 401(k)s became widely used as a primary retirement savings vehicle, a significant demographic shift means that many plans will find that they have—or will soon have—more retired/terminated participants than active employees in their 401(k) plans.

We can attribute this shift primarily to the huge effect of the retiring Baby Boomer generation as well as increasingly longer life expectancies.

According to the Pew Research Center, 10,000 Baby Boomers in the U.S. turn 65 every day, while 2018 U.S. Census Bureau data projects that there will be 73 million people aged 65+ by 2030, up from just 49 million in 2016. In terms of longevity, Social Security data indicates that today’s 65-year-old man can expect (on average) to live to age 84 and a woman can expect to live to age 88 – meaning roughly two decades in retirement.

DCIIA members aren’t alone in emphasizing the importance of this issue. The U.S. Government Accountability Office (GAO) has identified the need for improved options to aid employees reaching the retirement phase as one of its five strategic policy goals. The Bipartisan Policy Center’s Commission on Retirement Security and Personal Savings has also recommended that new rules be developed to encourage defined contribution (DC) plan sponsors to better engage retiring and near-retirement participants in decisions about lifetime income.

The Retirement Tier: It’s Not ‘All or Nothing’

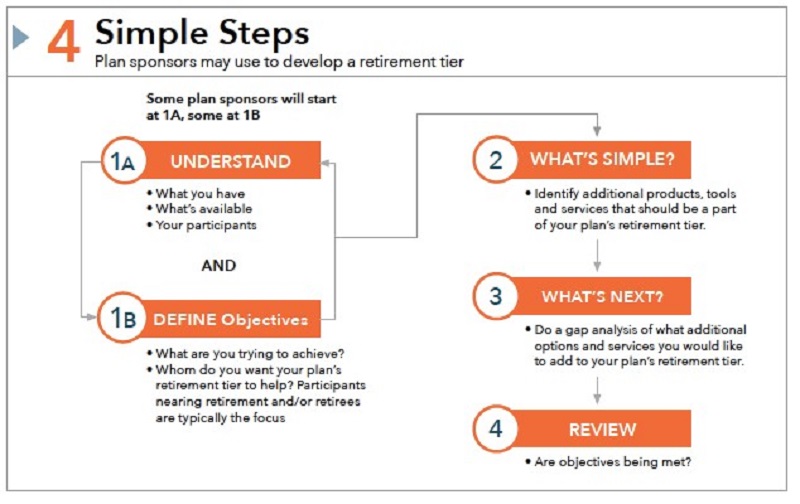

Most DC plan sponsors, participants and providers have historically focused on accumulating assets and savings. The “retirement tier” basically allows a DC plan sponsor to broaden the plan’s goal from one wholly focused on savings to one that also accommodates and supports participants who are near, entering or in retirement.

DCIIA recently published a series of focused white papers aimed at plan sponsors to help define and offer ways to build a retirement tier and encourage plan sponsors to:

- Learn how a retirement tier fits in with a plan’s investment tiers;

- Find out why the need to assist retirees and near retirees is being elevated in importance;

- Discover how to create a retirement tier; and

- Assess the pros and cons of a key retirement tier decision—whether, how and to what extent to allow/not allow retirees to stay in the plan and take partial withdrawals.

As to the last point in particular, DCIIA encourages plan sponsors to have candid discussions internally as to whether they do want to retain participants in the plan post-retirement. Once that decision is made, if the plan does want retirees to stay, it should be clearly and consistently communicated. This may allow participants to benefit from the lower fees and additional governance offered by their 401(k) plans relative to some retail retirement savings options.

DCIIA’s reports are intended to help plan sponsors determine plan participants’ actual distribution history, review how participants’ money can leave the plan and identify what percentage of them might benefit from having access to a retirement tier now or in the near future.

Debunking Misconceptions

In DCIIA’s discussions with plan sponsors, the group has identified some common misconceptions about the retirement tier, such as the idea that it needs to be:

- A silver bullet: All individuals have unique circumstances and a single solution is unlikely to adequately address all needs.

- In-plan: Plan sponsors choosing not to allow partial withdrawals can still provide meaningful assistance in the run-up to retirement.

- A separate (or new) tier of the plan: Many retirement tier components may already be in the plan.

- Recordkeeping intensive: Complex builds may not be required.

- An insurance solution: An insurance solution (such as annuities) is not a requirement, although annuities and other insurance-based strategies may be a beneficial part of a retirement tier.

It’s worth the time and effort to discuss and implement retirement tier solutions. In addition to the benefits for plan participants, retaining these participants’ assets even after they retire can assist DC plan sponsors in achieving and retaining plan economies of scale regarding recordkeeping and investment management fees.

Thoughtful plan design and communication around the post-retirement phase can also help to boost an organization’s reputation as an employer, supporting efforts to attract and retain top talent. This could also help to alleviate employees’ anxieties or uncertainties around their post-retirement finances— as seen in the illustration, a quarter of plan participants in a recent survey did not know what they would do with their 401(k) account savings at retirement.

America’s workers are increasingly being asked to make complex financial decisions on their own that will influence the rest of their lives. Employer awareness of these challenges as well as the implementation of initiatives such as 401(k) automatic features and financial wellness programs are helping to close the retirement savings gap.

For a retirement program to meet the goals of its entire constituency, it must address both the accumulation and distribution phases of retirement. A retirement tier enables a plan sponsor to focus on helping retired and nearly retired employees understand both how to invest and how to withdraw their savings in order to generate income that will support them during their retirement years.

Peg Knox is chief operating officer of the Defined Contribution Institutional Investment Association (DCIIA). Prior to joining DCIIA, she was the global retirement plans manager at a large corporation.

This feature is to provide general information only, does not constitute legal or tax advice, and cannot be used or substituted for legal or tax advice. Any opinions of the author do not necessarily reflect the stance of Institutional Shareholder Services or its affiliates.