Never miss a story — sign up for PLANSPONSOR newsletters to keep up on the latest retirement plan benefits news.

Benefits July 23, 2025

Public Pension Funds Stay Steady, Weather Tariff Stumble in FY 2025

State funds will make money this year but may miss their benchmarks, according to Equable.

Reported by

Matt Toledo

Many public pension funds have closed the books on their 2025 fiscal year, the one-year period that typically ends on June 30, and their investment returns are expected to hold up, continuing the third year of a market rally across asset classes, despite mid-year volatility.

A tech-fueled equity rally drove returns for many public funds. Between July 1, 2024, and June 30, 2025, the S&P 500 Index rose 12.8%.

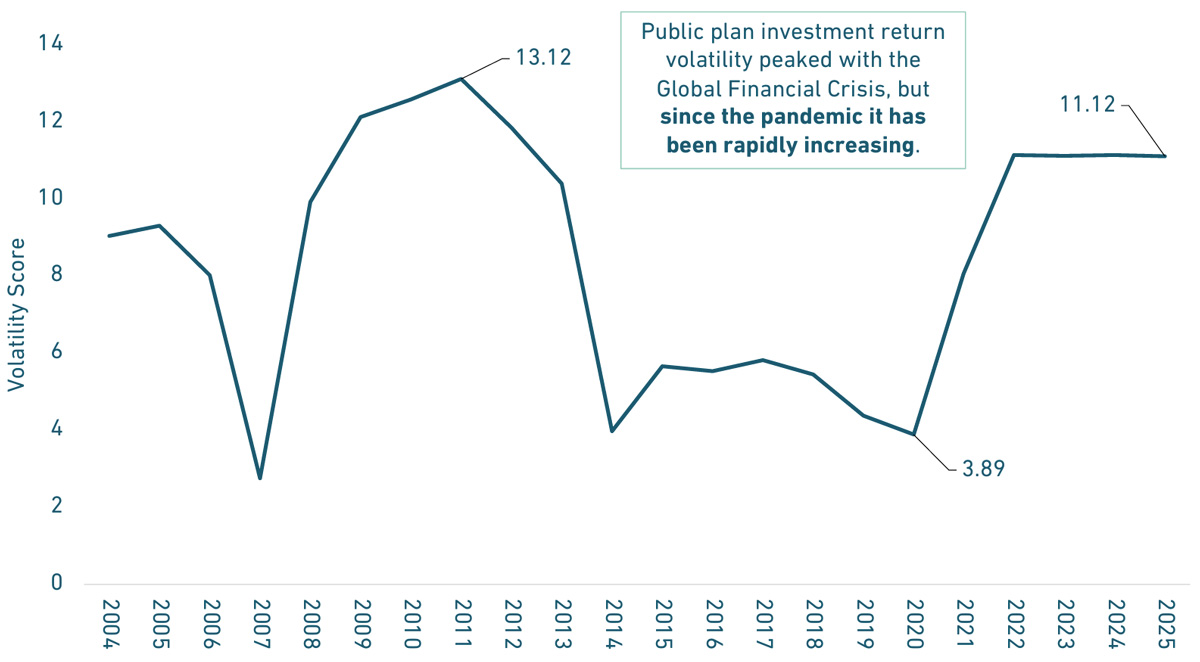

Increasing Investment Return Volatility

Volatility is near global financial crisis era levels

Note: From a technical perspective, volatility is measured using the standard deviation of the financial instrument being examined. In the case of investments, this can be done by calculating the standard deviation of the year-over-year returns.

Source: State of Pensions 2025, Equable Institute’s Annual Report 6th Edition

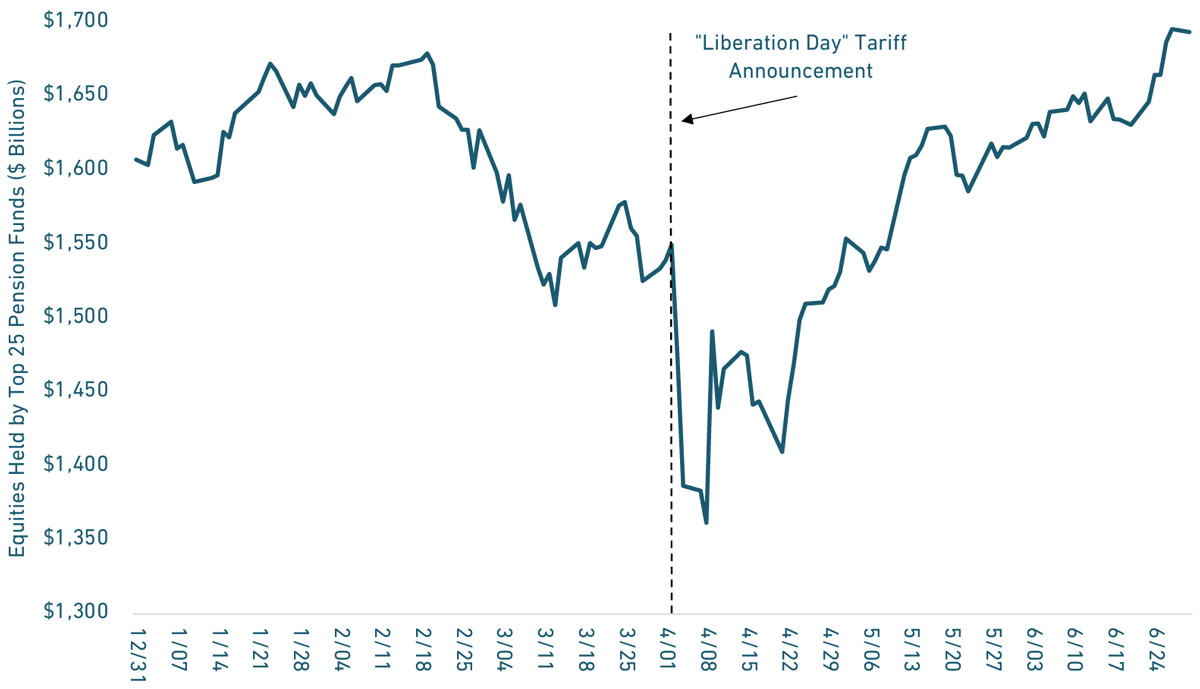

April’s rollout of President Donald Trump’s new tariff regime shocked the markets. A few days following the announcements, the largest public plans had seen the value of their equity portfolios fall by $170 billion, but by early May, markets had mostly recovered from those lows.

Public Pension Asset Volatility in 2025

Daily change in equity value, Top 25 pension funds | Jan 1 – Jun 30

Source: State of Pensions 2025, Equable Institute’s Annual Report 6th Edition

Several Funds Release Fiscal 2025 Returns

To date, few public U.S. funds have reported investment returns for fiscal 2025; they are typically announced later in the summer. The largest public pension fund in the U.S., the California Public Employees’ Retirement System, however, this week reported preliminary fiscal 2025 returns of 11.6%.

Several of Australia’s public and industry superannuation funds posted their fiscal 2025 returns in early July. Cbus’s main pension option, Cbus Growth MySuper, returned 10.29% during the one-year period that ended June 30. Its other investment options returned 11.80% and 11.68%, respectively, according to Financial Standard, a sister publication of CIO.

AustralianSuper reported a 9.5% return from its MySuper option, while the Australian Retirement Trust and HESTA reported returns of 11.2% and 10.18%, respectively.

But while U.S. public funds stemmed their losses from tariff-driven lows, they did not exactly make a full recovery “in the sense that April never happened,” says Anthony Randazzo, CEO and executive director of the Equable Institute, a nonprofit that studies and reports on retirement security in the public sector.

“There were missed opportunities,” says Randazzo, noting that, on average, state funds are going to miss their assumed rates of return for the last fiscal year. “They will make money this year, [but] they’re going to slightly underperform that particular benchmark.”

In Equable’s “State of Pensions 2025” report, released Wednesday, the firm projected an average investment return of 5.41% for fiscal 25, down from 9.7% in fiscal 2024.

These projected average returns are relative to an estimated average assumed rate of return of 6.87%, according to Equable, which tracked and projected the performance of 235 U.S. public pension funds.

According to Equable, the average assumed rate of return has declined from 8.07% in 2001 to 6.87% in 2025. In 2005, the median assumed return rate was 8%, falling to 5% in 2025.

Funded Status Stays Steady, but Challenges Remain

Equable predicted the funded status of U.S. public pension funds will improve to 81.4% through fiscal 2025, up from 78.3% at the end of fiscal 2024, based on a decrease in aggregate unfunded liabilities to $1.35 trillion from $1.51 trillion as a result of record high contributions. This would be the third consecutive year of improvement in public plan funded status.

However, the unfunded liability would remain relatively unchanged from 2009—when it was $1.9 trillion, according to Equable. Still, pension funds in 45 states saw their funded statuses increase. Only four states have plans with a funded status of less than 60%: New Jersey, Illinois, Kentucky and Mississippi.

Equable projects $7.23 trillion in pension liabilities in fiscal year 2025, against $5.88 trillion in assets. The gap between assets and liabilities was smallest in 2007; in that year Equable reported $3.27 trillion in pension liabilities and $3.01 trillion in assets.

Retirements Will Keep Benefit Totals Growing

Public pension cash flows are increasingly turning negative, because benefit payments are growing larger than contributions as the number of retirees grows and the number of active employees remains steady. According to Equable, there were 7.6 million retired and inactive members of public pension funds in 2001, while there were 12.7 million active employees.

By 2024, the number of retirees and inactive members more than doubled to 18.8 million, while active employees rose only marginally to 14.5 million.

“U.S. public pension plans are still stuck in pension debt paralysis. That’s why pension fund investment managers have maintained high-risk, high-reward bets even as contribution rates are near historic highs,” the Equable report stated. “Over the last five years pension funds have survived the Covid Pandemic and this April’s tariff-triggered financial market collapse—but that doesn’t mean pension funds have thrived.”

According to Milliman, the funded status of public pension funds in its Public Pension Funding Index, which includes the largest 100 public defined benefit plans in the U.S., increased by 2.4 percentage points to 81.1% at the end of May, as markets recovered from the tariff whiplash of April.

“May’s robust returns drove improvements in individual plans’ funding levels, with five plans lifted above the 90% funding mark—for a total of 30 plans now in this healthy range—and one plan rising above the 60% funding mark, leaving only 11 of the 100 PPFI plans below this critical benchmark,” said Rebecca Sielman, a principal in and consulting actuary at Milliman, in a statement.

« ERISA Complaint Alleges Mismanaged Plan Cost Participants $100M