For more stories like this, sign up for the PLANSPONSOR NEWSDash daily newsletter.

Investing February 8, 2021

Real Estate Investments Can Make a Difference in Retirement Savings Accumulation

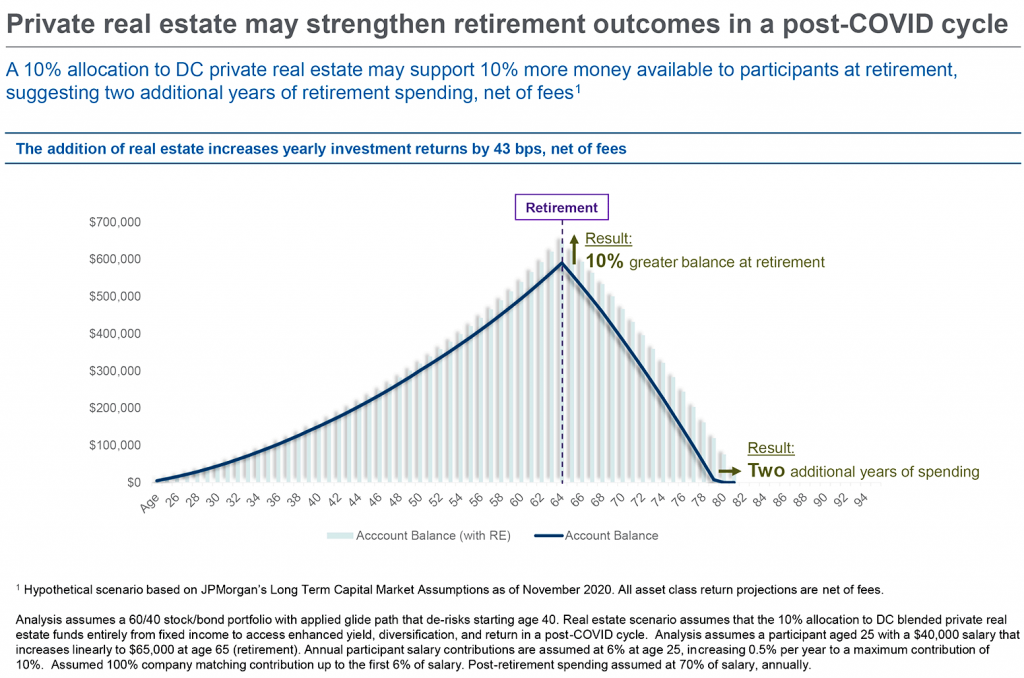

J.P. Morgan Asset Management says participants with a 10% exposure to real estate can expect a 10% greater ending balance at retirement.

Reported by

Lee Barney

Over the next 10 to 15 years, J.P. Morgan Asset Management forecasts that public equities will return 4% to 5% and U.S. aggregate will return approximately 2%, Pulkit Sharma, head of alternatives portfolio strategy and solutions at the firm, tells PLANSPONSOR.

“For a portfolio with a 60/40 allocation [60% to global equities and 40% to U.S. fixed income], the highest valuation projected returns are 4.2% a year,” Sharma says. “In this construct, real estate fits in nicely in the portfolio. U.S. core real estate is projected to return 5.9% over the next 10 to 15 years. That’s an approximate 2 percentage point premium over U.S. equities, a 4 percentage point premium over the U.S. aggregate and 1 percentage point premium over high yield. Also, real estate can actually grow with inflation. All of these reasons make it a powerful addition to a multi-asset portfolio.”

In fact, J.P. Morgan recommends that retirement portfolios have a 10% exposure to real estate and says this exposure will increase a retirement portfolio’s ending balance by 10%.

Jani Venter, director of defined contribution (DC) fund management team at J.P. Morgan Asset Management, adds: “Real estate is also a cyclical asset class, and we are currently in a trough. We expect it will rebound and continue to grow over the next 10 to 15 years.”

Venter also points out that just as defined benefit (DB) plans have embraced real estate, it makes sense for DC plan sponsors to include real estate in multi-asset, professionally managed funds, such as target-date or white label funds. In fact, Venter says, “one trend we have seen in the past two to three years is investors increasing their exposure to real estate. They are also including real estate in pre- and post-retirement income solutions.

“In the search for retirement income, especially with yields being so low and government bond returns even being negative, many investors are turning to real estate to deliver that income,” Sharma continues. “Real estate can play a role in both the early stages of a target-date fund [TDF]’s glide path and the late stages of its glide path as a fixed income substitute.”

In “Long-Term Capital Market Assumptions,” J.P. Morgan says, “The long-term outlook for real assets is attractive, particularly when considered on a risk-adjusted basis, relative to most traditional assets and financial alternatives. We expect core real assets to continue to gain traction in portfolios, give the stable and diversifying nature of their return streams, driven by income generated from long-term contractual cash flows backed by strong counterparties.”

« Plan Administrators Don’t Have to Scramble to Report Qualified Plan Loan Offset Amounts