Get more! Sign up for PLANSPONSOR newsletters.

Thought Leadership October 1, 2017

Fixed income: How active do you want to go?

Challenges to bond fund returns include rising rates, slow growth, political uncertainty, demand constraints and more. That’s why many defined contribution (DC) plan sponsors are exploring whether their plan’s fixed income choices are sufficient to meet the needs of participants.

Sponsored by BlackRock

Risk and the Agg

The Fed’s policy of normalization sounds reassuring. But, in practice, normalization may simply shift uncertainty from short-term rates to further along the yield curve. This uncertainty comes at a time when global competition for U.S. bonds, aging demographics and potential economic headwinds further complicate today’s fixed income market.

As a result, many plan sponsors are questioning whether bond exposures pegged to the Bloomberg Barclays U.S. Aggregate Index (“the Agg”) will meet participants’ needs. To help them answer the question, we will explore some of the challenges ahead for the fixed income market. The following article provides a snapshot of this analysis. For our full outlook, visit BlackRock’s DC site.

Where are the active management opportunities?

Complexity creates opportunity

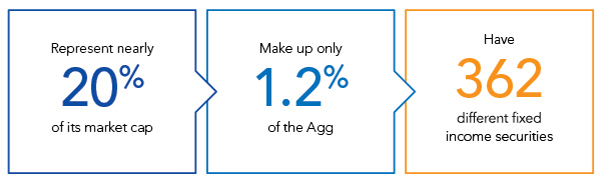

The top 10 companies in the S&P 500 represent nearly 20% of its market cap, yet they make up only 1.2% of the Agg.[1] What’s more, those 10 companies have 362 different fixed income securities. The wider fixed income market includes securities denominated in different currencies, with different maturities and underlying covenants. The intricacy of some structured products is sufficiently high that a portfolio manager may be able to generate alpha through security selection, independent of the direction of rates or credit spreads.

The top 10 companies in the S&P 500

Different investors, different objectives

Pension funds, bank portfolios, reserve managers, central banks and other market participants may have objectives other than maximizing income or mark-to-market returns. By understanding the motives of market participants, portfolio managers may recognize opportunities to generate alpha or manage risk.

Global demand helps drive U.S. market

Ten years ago, what investors in other countries did was not necessarily germane to the valuation of the U.S. yield curve. Today, it’s easy for a Japanese institutional investor to execute a trade for U.S. denominated debt. An active manager with a good grasp of global dynamics may be able to exploit external demand to the fund’s advantage.

Demand for fixed income continues to increase

Source: Federal Reserve, Bloomberg as of 4/17/17.

Aging population increases demand for income

A growing population of retirees is driving demand for safe, reliable income at a time when global yields are very low. Active managers may be able to better respond by targeting areas of the yield curve or investing in income-producing instruments beyond what is traditionally captured by the Agg.

Tools of active management

Duration

Perhaps the most obvious way to manage interest rate risk is by extending or reducing duration. Current duration of the Agg is 5.72 years.[2] If an active manager is given 40% flexibility in setting a duration target, it would translate into a range of approximately 3.5 to 7.5 years. Even if the mandate requires matching the duration of the Agg, an active manager may not need to own duration in equal doses across the curve. Different positions can be established in order to avoid the areas the manager thinks are most susceptible to price decline.

Credit quality

Given flexibility to go beyond investment grade to include high yield, asset-backed and other securities, active managers can pursue risk-adjusted return ideas across the yield curve, while still keeping the performance consistent with the Agg over different market cycles. This flexibility can be constrained to a percentage of the portfolio, or it can be completely unconstrained within an absolute return or income mandate.

The choice is ultimately a matter of the plan sponsor’s objectives, investment policy statement and investment outlook.

What now?

The average DC plan offers 22 to 24 fund choices, of which fewer than three are fixed income. A case can be made that the attention given to fixed income within the core menu needs to increase.

We’ve developed some key questions to ask as you evaluate your fixed income options. For these and more, visit BlackRock’s DC site.

Investing involves risk, including possible loss of principal.

This material is provided for educational purposes only. Moreover, it neither constitutes an offer to enter into an investment agreement with the recipient of this document nor an invitation to respond to it by making an offer to enter into an investment agreement.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of September 2017 and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. Reliance upon information in this material is at the sole discretion of the reader.

Asset allocation and diversification strategies do not guarantee profit and may not protect against loss. Past performance is no guarantee of future results.

No part of this material may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, recording or otherwise, without the prior written consent of BlackRock.

The information contained in this presentation may contain commercial or financial information, trade secrets and/or intellectual property of BlackRock.

FOR INSTITUTIONAL OR PROFESSIONAL USE ONLY.

©2017 BlackRock, Inc. All Rights Reserved. BLACKROCK is a registered trademark of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.

MKTG0917U-261392-781455

[1] Source: BlackRock, data as of January 2017.

[2] Source: BlackRock. As of 6/30/17.