Get more! Sign up for PLANSPONSOR newsletters.

Opinions August 10, 2020

Barry’s Pickings: Retirement Finance and the Bonds Between Generations

Michael Barry, president of O3 Plan Advisory Services LLC, discusses how the “circle of life” relates to retirement security.

Art by Joe Ciardiello

“How sharper than a serpent’s tooth it is to have a thankless child!”—Shakespeare, King Lear

Retirement is such an ancient human challenge. As humans, we are faced with two bookends of dependency. As children, we are utterly dependent on our parents. And in our old age, we are utterly dependent on our children—or at least that is how it used to be. We have, over the last 150 years “socialized” these burdens to some extent (e.g., through state education and daycare and through Social Security) and, with respect to retirement, developed “utilities” (e.g., retirement plans) that permit us to some extent to provide for our own retirement.

But let us imagine: a stone age hunter who manages to live a long life wakes up one morning to discover that he can’t hunt any more. Unless he has a child (or there is someone else’s child) willing to care for him (e.g., hunt for him), he is out of luck.

To a large extent that was how things worked for most of human history. And we developed a set of norms/values that emphasized this need for reciprocity between generations. The obligation on the part of parents to care for their children and for children to care for their parents.

Thus, the fifth commandment: “Honour thy father and thy mother: that thy days may be long upon the land.” (Exodus 20:12, KJV) You are to honor your parents (as a child) so that you may live a long life (e.g., in retirement). Reciprocity. Most cultures developed this reverence for the old, rooted in the child’s gratitude for the care her parents had given her.

It struck me, in talking to my son about King Lear, that this play was literally about retirement—and the dependence of the old on the young. Lear wants to stop working at his job (as king) and expects his daughters to take care of him. And Shakespeare’s subject is: where the relations between parent and child are disordered, retirement may become an existential catastrophe.

But, the Singularity

All of this is very biological. And we are living in an age in which the goal of many is, for very understandable reasons, to use technology to transcend biology. Most radically, in the pursuit of the singularity—consider Ray Kurzweil’s book “The Singularity Is Near: When Humans Transcend Biology.” Understandable in that this effort is driven mostly by a desire to relieve human misery and extend human life. So that our days might be long upon the land.

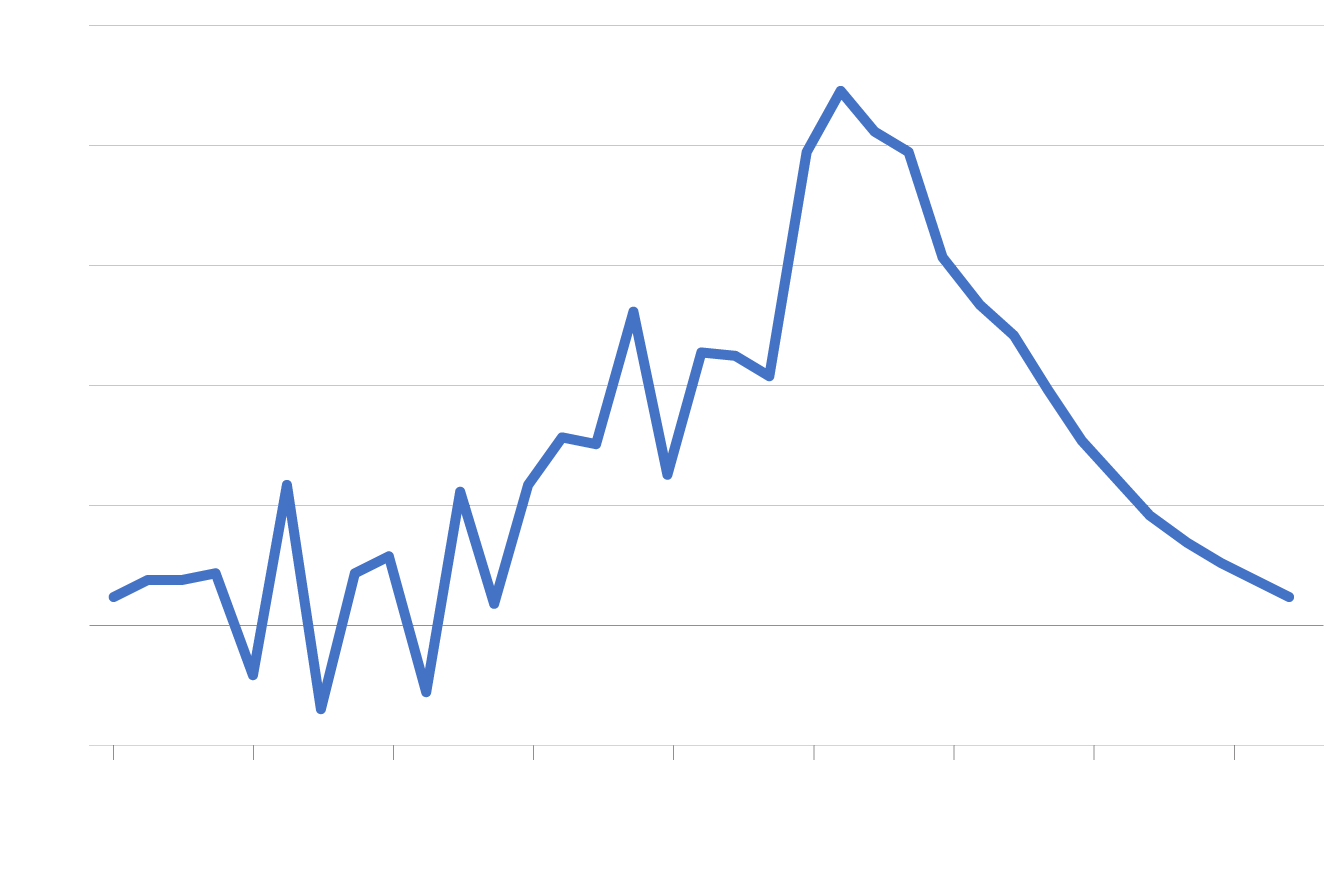

So, what happens when (as in our current situation) we stop having as many children as we used to, and there are (relatively) fewer children to care for more old people? Here is a chart of the rate of growth of the human population from the year 1000 projected to the end of this century.

Annual Rate of World Population Growth (Year 1000 – 2100)

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

-0.5%

1300

1800

1960

2040

2080

1000

1600

1920

2000

Years

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

-0.5%

1300

1800

1960

2040

2080

1000

1600

1920

2000

Years

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

-0.5%

1300

1800

1960

2040

2080

1000

1600

1920

2000

Years

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

-0.5%

1300

1800

1960

2040

2080

1000

1600

1920

2000

Years

Source: Retirement Savings Policy—Past, Present, and Future, Michael Barry (De|G PRESS, 2018)

When we consider the implications of this trend for retirement finance, one question is, which way does the causal arrow point here? Does the precipitous decline in population growth (beginning around 1970) reflect an increase in our ability to provide for ourselves in retirement, through the development of state-mediated old-age security programs and private retirement plans? Or is the development of those retirement savings programs a response to the decline in population growth?

Interestingly, that super-algorithm—the use of technology to transcend biology—is crucial to this process. Because without technological progress, retirement saving, whether state-mediated or private, we will not solve the problem of retirement. Here’s the simple version: if, in the future, you have fewer working people and no increase in (future) productivity, you will be poorer. You’ll just be paying a smaller number of (young, working) people a whole lot of money to take care of you. Thus, there is no “real” retirement saving unless the money saved is turned into increased future productivity—either through increased population or improved technology.

The Need for a Bond Between Generations Never Disappears

Moreover, even if “the singularity is near,” we are still going to need those norms/values—the reverence for the old, rooted in their care for the young. Because the old will still (in the end) be dependent. And without that emotional bond between generations, there will be nothing to stop young people from simply adopting different priorities—different from keeping their parents alive—and turning off the machines sustaining them to save energy. Not everyone sees a large old-age population as a good thing.

Indeed, retirement savings programs can (in fact) exacerbate this challenge, of preserving the bonds between generations. Particularly in a period of declining population growth. Because, to “save for retirement,” assets must necessarily be diverted away from the young. This is easier to see at the macro level, with respect to state-mediated pay-as-you-go retirement systems, where younger, working people must, in a period of declining population growth rates, pay more and more to provide old age security benefits to their parents.

But it also happens at the micro level—e.g., in the reduction of the legacy that parents leave their children, instead consuming that legacy in retirement spending.

And, of course, the ultimate diversion of resources from the young to the old is to just not have any children. So you can save for retirement. I hope the emptiness of such a strategy, if implemented at the level of society-as-a-whole, is transparent.

In these conditions, the need for that deep, close bond between parent and child is, if anything, even more acute.

At the risk of imposing on my readers, I would like to conclude with this meditation by George Oppen (from his poem “Of Being Numerous”) on this mystery (the same subject as Shakespeare’s Lear):

We seem caught

In reality together my lovely

Daughter,

…

And in the sudden vacuum

Of time ...

... is it not

In fear the roots grip

Downward

And beget

The baffling hierarchies

Of father and child

As of leaves on their high

Thin twigs to shield us

From time, from open

Time