For more stories like this, sign up for the PLANSPONSOR NEWSDash daily newsletter.

Benefits December 9, 2022

Bipartisan Group Introduces Bill for Portable Federal Retirement Accounts

Legislation would establish a new program to give eligible workers access to portable, tax-advantaged accounts.

Reported by

Amy Resnick

U.S. Senators John Hickenlooper and Thom Tillis and Representatives Terri Sewell and Lloyd Smucker Friday introduced the Retirement Savings for Americans Act, to create a program that would give American workers access to portable, tax-advantaged retirement savings accounts, with federal matching contributions for certain low- and middle-income workers.

The proposed savings program would offer investments similar to those offered to federal and military workers in the Federal Retirement Thrift Savings Plan. The proposed bill anticipates providing a menu of low-fee investment options, including target date funds tied to a worker’s estimated retirement date and stock and bond index funds, according to information from Hickenlooper’s office. The federal match would be a federal income tax credit, according to the draft bill.

Smucker, R-Pennsylvania, said the bill is intended to advance the pending SECURE 2.0 legislative package and build on it when the Retirement Savings for Americans Act is reintroduced in the next Congress.

“Too many Americans are working their entire adult lives only to reach retirement and find they don’t have enough saved,” Hickenlooper, D-Colorado, said in a release. “Helping people save is an easy, efficient way to cut income inequality while making sure all workers get the retirement they’ve earned.”

Co-sponsor Tillis, R-North Carolina, added, “Roughly 40 million Americans lack access to an employer-sponsored retirement plan, which represents a significant roadblock to achieving financial security for their retirement.”

Sewell, D-Alabama, and Smucker are co-sponsors in the House.

“This critical, bipartisan legislation would address serious gaps in our retirement system and make it easier for low- and middle-income workers to save for retirement,” Sewell said in the statement.

This legislation is aimed at providing retirement savings accounts to the up to 60% of U.S. workers that lack access to an employer-sponsored retirement plan, according to information from Hickenlooper’s office.

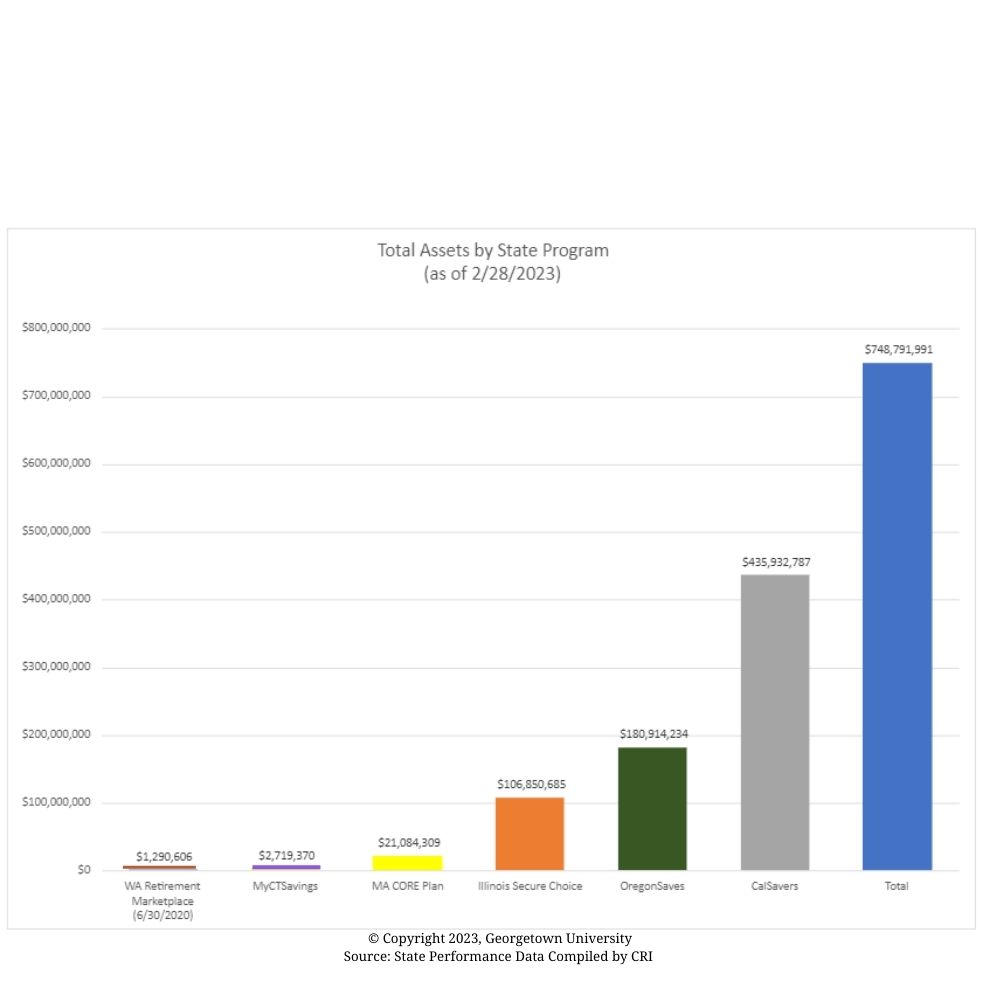

Many states have launched state-sponsored programs to enable workers without access to an employer-sponsored plan to save. In recent years, workers have saved more than $574 million through such state programs, according to information from the Center for Retirement Initiatives at Georgetown University. The largest state-sponsored programs are CalSavers, OregonSaves and Illinois Secure Choice. Overall, there are 16 state-sponsored programs and two city-sponsored programs.

The state and local programs do not offer matching contributions.{kind=link}

Information provided by Hickenlooper’s office says the federal Retirement Savings for Americans Act contains the following provisions:

- Eligibility and auto enrollment: Full- and part-time workers who lack access to an employer-sponsored retirement plan would be eligible for an account, and they would be automatically enrolled at 3% of their income. They could choose to increase or decrease their withholding or opt out entirely at any time. Independent workers (including gig workers) would also be eligible.

- Federal contribution: Low- and moderate-income workers would be eligible for a 1% automatic contribution (as long as they remain employed) and up to a 4% matching contribution via a refundable federal tax credit. This would begin to phase out at median income.

- Portability: Accounts would remain attached to workers throughout their lifetimes, and workers would be able to stop and start contributions at will.

- Private assets: The accounts would be the property of the worker, and the assets could be passed down to future generations to help them build wealth and financial security.

- Investment options: Much like the current Thrift Savings Plan, participants would be given a menu of simple, low-fee investment options to choose from, including lifecycle funds tied to a worker’s estimated retirement date and index funds made of stocks and bonds.