For more stories like this, sign up for the PLANSPONSOR NEWSDash daily newsletter.

Opinions October 14, 2020

Retirement Income: Spotlight on Annuities

Peg Knox, with the Defined Contribution Institutional Investment Association (DCIIA), discusses what plan sponsors should consider before implementing an income solution.

Many active plan participants are already thinking about retirement income. In a 2018 Defined Contribution Institutional Investment Association (DCIIA) white paper, we cited data from a Cerulli survey of active plan participants that found “developing monthly income from my investments” was the second-highest priority when asked about most important topics in retirement planning. The top priority was “health care expenses.”

Retirement income solutions cover a wide spectrum of insurance and investment products that can address different participant needs, whether they are in the savings or spending phase. The solutions are intended to help participants while maintaining the benefit of institutional oversight and pricing. There are both in-plan and out-of-plan solutions that may be guaranteed or non-guaranteed.

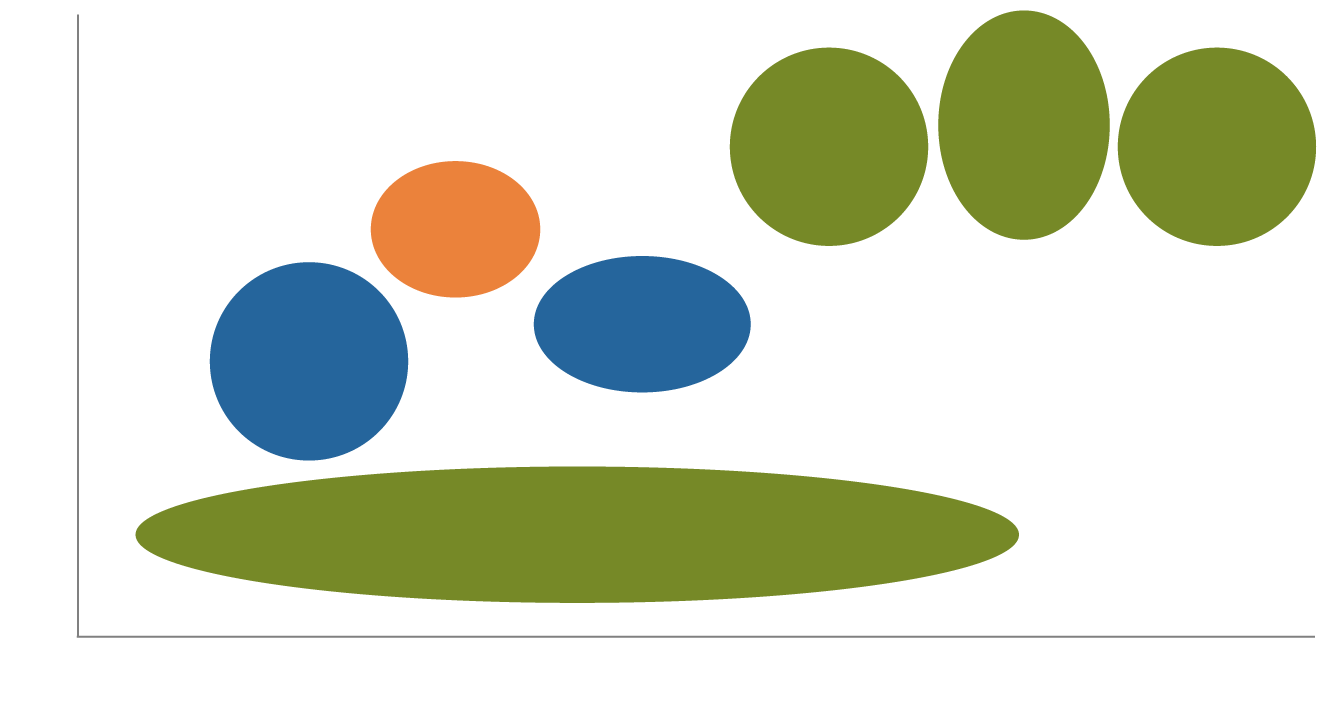

Callan also demonstrates how various retirement income products balance complexity and predictability in the following illustration, noting, “when reviewing the options, plan sponsors should evaluate the breadth of choices they wish to offer retirees, alongside the level of fees and complexity.”

Income Predictability

Qualified Longevity Annuity Contract

Guaranteed Minimum Withdrawal

Benefit

Annuity

Stable Value

Managed Account

Target Date Retirement Income

Managed Payout

Complexity

Income Predictability

Guaranteed Minimum Withdrawal

Benefit

Qualified Longevity Annuity Contract

Annuity

Stable Value

Managed Account

Target Date Retirement Income

Managed Payout

Complexity

Income Predictability

Guaranteed Minimum Withdrawal

Benefit

Qualified Longevity Annuity Contract

Annuity

Stable

Value

Managed Account

Target Date Retirement Income

Managed Payout

Complexity

Income Predictability

Qualified Longevity Annuity Contract

Guaranteed Minimum Withdrawal

Benefit

Annuity

Stable

Value

Managed Account

Target Date Retirement Income

Managed Payout

Complexity

Source: “DC Plans Have Helped Participants Save. Now They Need to Help Them Spend,” Callan, August 2018.

Readers will note that annuities—which are seeing renewed interest since the Setting Every Community Up for Retirement Enhancement (SECURE) Act’s safe harbor was enacted for plan sponsors regarding annuities selection—rank highly both in predictability and complexity. This effectively highlights the main issues with annuities: They can be seen as confusing and expensive, but also offer highly sought-after predictable retirement income. There are many nuances when it comes to types of annuities, but we would like to highlight two here.

Immediate or deferred annuity: When a plan offers this distribution option, a participant may purchase an annuity from an insurer that makes periodic payments. The income payments can begin either within 12 months (i.e., “immediate annuity”) or at a later date—typically three to five years later (i.e., “deferred income annuity”). Such annuities might be attractive for a participant who wants a secure income but does not want to begin retirement benefits yet. Annuity strategies can be based on single or joint lives, and payments can be made for life, a designated period or a combination of both. These allow participants to create an income stream similar to those provided by defined benefit (DB) plans.

Qualified longevity annuity contract (QLAC): Introduced by the Department of the Treasury and the IRS in 2014, a QLAC provides the participant with the opportunity to purchase, within defined limits, a very simple, inexpensive deferred income annuity that will guarantee income at older ages. This enables participants to adopt a spending plan for their savings until their average life expectancy, and to have an income guarantee if they live longer than the average. Typically, these income payments begin by age 85.

Plan sponsors should work as needed with their counsel to amend their plans, with their advisers to update plan policy statements and with their recordkeepers and other service providers to ensure that their plans’ infrastructure and providers can support any changes. One approach to consider is the “retirement tier” framework, which DCIIA has defined as a range of products, solutions, tools and services that allow a plan sponsor to broaden the plan’s goal from one wholly focused on savings to one that also accommodates and supports participants who are near, entering or in retirement.

Consider how your organization would answer the following questions:

Initial considerations:

- What is the typical participant profile (age, contribution rate, tenure)?

- What are the plan’s goals regarding income?

- What is the plan’s appetite for providing retirement income strategies?

Income solution considerations:

- What types of retirement income solutions are available?

- What are the trade-offs with the different solutions?

- How does the product fit the participant population and plan demographics?

- Does the solution qualify as a qualified default investment alternative (QDIA)?

- Are the fees associated with the product reasonable?

- What support—for instance, planning and tools or access to advisers—is available to participants?

Fiduciary considerations:

- How are you planning to fulfill and document your fiduciary responsibilities, or will you obtain third-party investment advice or delegate some or all of your responsibilities to a 3(38) investment manager?

- What are the counterparty risks associated with products that have an embedded guarantee? What other risks should be considered?

- What process will you use for ongoing monitoring?

- Is there a benchmark for the product or solution?

- What changes to your plan’s investment policy statement (IPS), summary plan document (SPD) and other plan documents would be appropriate?

Operational and administrative considerations:

- Can your current recordkeeper administer the retirement income solutions you’re considering?

- Are solutions portable at both the plan sponsor and participant levels?

- What choices are available if you decide to stop offering the solution or replace the provider?

Participant outcomes:

- How will you educate participants about the retirement income solution?

- What is the expected potential impact on retirement outcomes for participants?

- How will you measure success?

One of DCIIA’s core beliefs is that the primary role of defined contribution (DC) retirement plans is to create retirement income adequacy. Access to retirement income products, education, planning tools and advice have the potential to significantly improve participant retirement outcomes. In particular, regarding annuities, the recent protections offered by the SECURE Act may make it worth taking a second look at whether they might be appropriate for your retirement plan.

Peg Knox is the chief operating officer (COO) of the Defined Contribution Institutional Investment Association (DCIIA) and is a former plan sponsor. Additional resources on this topic are available in DCIIA’s Resource Library.