Never miss a story — sign up for PLANSPONSOR newsletters to keep up on the latest retirement plan benefits news.

Thought Leadership September 26, 2014

Economic Cost vs. Accounting Cost

Maybe Annuities Aren’t That Expensive After All

Sponsored by

Pacific Life

Defined benefit (DB) plan sponsors have been contemplating various pension de-risking solutions more seriously than ever. Some plan sponsors have the preconceived idea that annuities are “too expensive.” But many plan sponsors have not considered, and have not measured, the true economic cost of their defined benefit pension plans. To further investigate the concept of accounting cost vs. economic cost, Alison Cooke Mintzer, editor-in-chief of PLANSPONSOR, spoke with Russ Proctor and Marty Menin, both directors of institutional sales at Pacific Life. They explained the difference between these two types of costs.

PS: What is a plan sponsor’s accounting cost?

Proctor: Accounting cost refers to the amount of liability the plan sponsor has to report on its balance sheet for its defined benefit (DB) plan. This pension accounting liability is the present value of only the projected benefit payments that the plan sponsor promised to the pension plan participants. It does not include a variety of other direct or indirect expenses that the plan will pay in the future but that the plan sponsor is not required to recognize on the balance sheet now.

PS: What’s the difference between that and the economic cost?

Menin: Economic cost refers to the all-in total present value of the costs that the plan sponsor will eventually pay for the maintenance of the pension plan. The direct expenses the plan sponsor pays includes for example: the annual administrative costs, actuarial costs, legal costs, asset management fees and Pension Benefit Guaranty Corp. (PBGC) premiums. Then there are indirect costs for which the plan sponsor may not receive an invoice that need to be recognized as part of the economic costs of the plan.

PS: Can you provide a little more detail about some of those indirect costs?

Proctor: An example of indirect cost is downgrades or defaults on bond investments. If the plan assets are invested in a bond that is downgraded or that defaults, then the plan assets will decrease. However, the plan sponsor does not receive a specific invoice identifying this cost. Another example is mortality improvement. The Society of Actuaries is releasing a new mortality table this year that indicates people are living longer. If participants live longer than expected, then the plan will have to pay benefits for a longer period of time, which will result in additional cost to the plan sponsor. This cost may not be realized in the accounting cost until the plan sponsor updates the mortality assumption. It is expected that the new mortality table could increase the liability 4% to 10%, depending on the age of the participants, compared with the table currently used in determining accounting costs.

Although some of these indirect costs such as default risk and mortality can be quantified and added to the economic costs, others are more difficult for plan sponsors to nail down. For example, there is a cost for the time spent by staff to research questions by participants, search for lost participants, conduct a search for a new asset manager, monitor and reconcile actual and expected investment results, etc. Indirect costs include the amount of time executives spend on all these things that take time away from managing the company’s core business. Clearly their time is valuable but nobody is quantifying that expense.

There are many costs that plan sponsors just take for granted as part of operating the pension plan. Accounting rules don’t require you to book those on your balance sheet, but you’ve got to take those into consideration when de-risking and comparing to the annuity costs.

PS: If a plan sponsor were to add in all of these additional costs you mention, how much higher is its economic cost relative to its accounting cost?

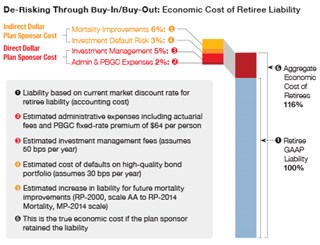

Menin: It will vary from plan to plan but could be about 16% higher than what the plan sponsor will show on their balance sheet. The chart we included here shows that, for an average plan, the present value of the future administrative costs, including PBGC premiums, is projected to add about 2% to the economic cost. Future investment management fees (based on a charge of 50 basis points [BPS] per year on assets under management [AUM]) would increase costs another 5%; mortality improvements are assumed to add another 6%; and finally the cost of default protection will add a few percent. Add these up and your true economic cost may be about 16% higher than the accounting cost disclosed on the balance sheet.

The important part of this is that plan sponsors need to analyze these future costs of maintaining the plan and add them to the current accounting liability.

Whether a plan sponsor believes that its total economic costs are 116% of the accounting liability, as we described, or lower, or higher, it’s vital to recognize that these costs are real. Plan sponsors need to be conscious of this when they compare their all-in plan costs with the costs of purchasing an annuity contract, to transfer the risk to an insurance company and de-risk their plan.

PS: How does that 116% compare with the cost of an annuity?

Proctor: It depends on several participant and economic factors. For example, for a group of retired plan participants, we often see annuity quotes that may range anywhere from 108% to 118% of their accounting liability. This cost is affected by the duration of the annuity contract. Are these people younger or older? How healthy is this group of participants? What industry are they in? The current interest rates at the time they actually purchase the annuity will affect the cost, as well. Costs are typically higher for active or terminated vested participants than for retired participants. This is due to longer duration of the liability, which includes reinvestment risk and more uncertainty of when the payments will commence.

Menin: For a long time, people just said, “Annuities are too expensive,” but often no one really sat down and crunched the numbers for comparison to the economic cost.

When the plan sponsor reviews the full calculations, they may find that it is often less expensive on a true economic basis to annuitize and transfer the risk to an insurance company.

Proctor: As we talk about comparing your economic

cost with the annuity cost, it’s also important to look at segments of the

plan. Sometimes we see that the annuity cost is much lower than the economic

cost might be for a group of retirees with very small benefits. The

administrative costs for those small benefits may be 8% to 10% of their

liability. So when you look at that small group, your economic costs may be

125% of the liability. If you can purchase annuities at 108%, you can have some

significant savings on pockets of participants within your plan—you can pull

out pieces of it, shrink the size of your plan and de-risk it in a very

economical way. n

Pacific Life, its distributors, and respective representatives do not provide any employer-sponsored qualified plan administrative services or impartial investment advice and do not act in a fiduciary capacity for any plan.