For more stories like this, sign up for the PLANSPONSOR NEWSDash daily newsletter.

Thought Leadership August 22, 2013

Looking for a Helping Hand

How plan sponsors

can help pre-retirees feel more secure about their impending retirement

Sponsored by American Century Investments

Are your plan participants approaching retirement age actually going to retire when they turn 65? Increasingly, at employers all over America, the answer to that question is no. Although many Americans would like to retire or at least start cutting back on work at that age, they cannot afford to. Diane Gallagher, Vice President, defined contribution investment only (DCIO) practice management at American Century Investments®, spoke with Alison Cooke Mintzer, Editor-in-Chief of PLANSPONSOR, on how these plan participants nearing retirement age feel about their efforts to save and their employers’ help along the way.

PS: In your recent research of how pre-retirees—those age 55 to 65 and employed full-time—feel about their retirement readiness, what did you find to be the most significant results?

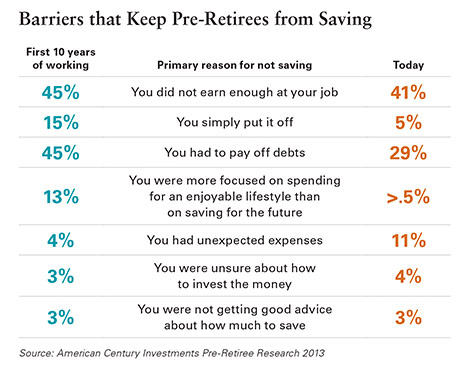

Gallagher: There are three major findings in this research. First, this group of working Americans has serious regrets about their savings efforts over the course of their careers. The biggest barrier to saving was the perception that they couldn’t afford it.

A second major finding is really about redefining affordability and helping people make solid spending choices early on. They told us, “I wish I could talk to my younger self about the decisions I was making.”

Finally, the third thing was not a surprise to anyone who works with defined contribution (DC) plans: Plan sponsor decisions have significant influence. Plan structure, design features, services and communication programs matter greatly. What participants can and can’t afford comes down to household budgeting. This group of pre-retirees needed help with budgeting and overall financial wellness.

Historically, the industry has put significant effort into communication and education programs for DC plans. Traditionally, those campaigns have focused on investing and the value of the employee benefit. We really need to teach people how to budget to make sure that there’s a little left over to save. Pre-retirees told us, “I would have made different spending choices. I wish I would have known the impact those decisions would have made on what I have saved today.”

PS: Were there any other barriers to pre-retiree success?

Gallagher: There’s a list: They didn’t earn enough, they just put it off, they were trying to pay off debt first, or they were spending on more immediate needs. Daily life got in the way.

Saving for the future is the easiest thing to put off.

You can’t put off a mortgage payment. You can’t put off buying your kids shoes that fit. Someone in their 30s might believe, “I can wait a little bit on this.” The reality is they can’t. More than a quarter of participants in our study said they didn’t start saving for retirement until they turned 40, that’s a lot of time to make up.

PS: What else did the research show about the role of the employer?

Gallagher: We asked pre-retirees to grade their employers on the retirement plan and the types of services offered with it. They graded employers higher on offering a plan, choosing a provider, selecting investments and administering the benefit. The higher grades were all about the mechanics of the plan.

We saw room for improvement on the support of that plan, especially with communications and education. Interestingly, plan sponsors and providers spend most of their blood, sweat and tears on developing communication campaigns and related tools. But are the materials covering the right content?

The typical communication programs focus on investing. We teach people about the investment options in the plan, about the difference between growth and value investing and telling them “don’t put all your eggs in one basket.” Should we address another topic?

This group of participants was saying, “Help me find a way to save.” It goes back to that idea of helpful budgeting and making better choices. If the median salary in the U.S. is $45,000, start there and say, “Here’s a sample budget. Here’s how you do it.”

Automatic programs are incredibly powerful, and pre-retirees acknowledged that setting up these guardrails would have helped them. Some 73% said automatic escalation would have had a positive impact on their savings. This group has regrets about not saving enough, and they are self-aware in acknowledging that certain strategies (like automatically increasing how much they were saving) would have helped. We didn’t hear any implication of blame; it was almost like “save me from myself.”

In terms of communication and education, the majority said that employers should require attendance at meetings about the plan, which was interesting because plan sponsors are often reluctant to mandate attendance. The majority of people said we just should require people to participate in plan meetings once a year to hear.

Nothing is important until it’s important. For this group, retirement is suddenly important. They’ve got a date on the calendar, and they’re taking an assessment right now.

PS: So what are plan sponsors doing, and what can they do to then help these participants?

Gallagher: The big lesson is to take advantage of how people make—or don’t make—decisions. Use defaults at higher contribution rates and include automatic escalation. You can’t default people at 3% and leave them there and expect them to have enough to retire. Start them higher and keep adding that 1%. That will make the difference. The key is the power of defaults.

We learned that leaving people to their own devices isn’t going to help them succeed. We need to put up the right guardrails, and the majority of people will stay within the guardrails. In that case, we’re giving them the best chance to be successful and to reach their retirement goals.

PS: When you put in some of these automated elements, often people think they can do that at the elimination of education. That really can’t be the case.

Gallagher: They still go together, but I’ve done employee communications for over 20 years. Plan design has to come first. You have to set up a good foundation and then use communication and education to address specific issues.

Plan sponsors tell me, “I want higher participation, I want higher deferral rates, and I want better asset allocation.” But if they’re not willing to make plan design decisions that support those, they are not going to be satisfied with results from a really broad communication program. Communication campaigns are most effective with a very targeted, surgical approach to addressing a specific issue. For example, a campaign might address helping people find ways to save, as we’ve discussed, or beginning the transition process to retirement. Those single-focus programs can bring strong results with a solid plan design as the base.

©2013 American Century Propriety Holdings, Inc. All rights reserved.