Never miss a story — sign up for PLANSPONSOR newsletters to keep up on the latest retirement plan benefits news.

Benefits November 14, 2013

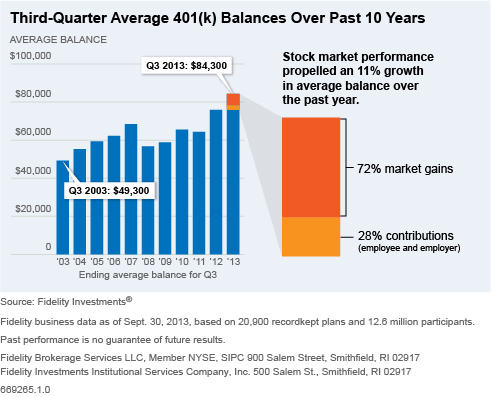

Average 401(k) Balance Sees Increase

November

14, 2013 (PLANSPONSOR.com) – Fidelity Investments says the average balance of

its 401(k) plan accounts rose to a record high of $84, 300 at the end of the

third quarter.

Reported by

Kevin McGuinness

That is an increase of 11.1% from last year, according to the 401(k) provider, and largely the result of a resurgent stock market. Fidelity’s analysis also found that employees who were continuously active in their 401(k) plan over the last 10 years saw average balances jump 19.6% to $223,100 during the past year. For preretirees, age 55 or older, who have been active in their plan for at least 10 years, the average balance is now $269,500.

Fidelity also found that with the increased adoption and availability of target-date funds and managed accounts in workplace retirement plans, one out of three employees now utilize a professionally managed investment option for 401(k) assets. This is a change from a decade ago, when nearly all plan participants were “do-it-yourself” investors and made the bulk of their investment decisions completely on their own.

“Today’s 401(k) plan is profoundly different than it was a decade ago,” says James MacDonald, president of workplace investing at Fidelity. “Plan design has evolved greatly to reflect the fact that 401(k) plans are often the primary driver of retirement savings for most working Americans. Professionally managed investment options can help working Americans achieve better retirement outcomes by creating a diversified portfolio, which is often the most challenging aspect of participating in a workplace retirement plan.”

The Fidelity analysis found that the population of participants who are choosing their own investment lineup has dropped dramatically with the rise and use of target-date funds and managed accounts.

At the end of the third quarter, one-third (33.1%) of 401(k) participants had 100% of their plan assets in a target-date fund, up from 3% just 10 years ago. Fidelity says the appeal of TDFs to participants is that such professionally managed mutual funds provide an age-based, diversified portfolio that gradually becomes more conservative as a participant nears, and then enters, retirement.

For younger Generation Y participants, 55% had all of their assets in a target-date fund, providing this population with a considerable improvement in their age-based asset allocation over prior years.

The analysis also shows that as participants age or build larger balances, they may be faced with more complex and competing financial needs. For these participants, a professionally managed account can provide an experience that takes into consideration assets outside their 401(k), such as an individual retirement account (IRA), pension or spouse’s savings, as well as an investor’s varied risk tolerances and retirement dates.

Since the third quarter of 2009, Fidelity has seen a more than three-fold increase in the portion of employers offering managed accounts to their employees, as well as the number of participants taking advantage of the service. In addition, assets in retail managed accounts such as IRAs or individual brokerage accounts have more than doubled since then. An infographic displaying information about third quarter average 401(k) balance over the past 10 years can be seen here.

{kind=link}

“A managed account acknowledges that some participants prefer a more personalized approach with their investment strategy based on their specific needs, including their emotional tolerance for risk or assets outside their 401(k),” MacDonald says.

As to what plan sponsors can do in light of this growth of “do it for me” participants, many have already adopted investment options, such as target-date funds, that better suit this hands-off approach, Jeanne Thompson, vice president of market insights at Fidelity, told PLANSPONSOR.

“After the release of the Pension Protection Act and the impact of the recession, many people found that they didn’t have the stomach for investment decisions," Thompson says. "Now we are seeing a more hands-off approach, with people realizing that they don’t have the skills or time to make such decisions on their own.”

In terms of plan design, says Thompson, plan sponsors can help these participants by adding automatic enrollment and defaulting them into a fund. With younger participants, she adds, it is not so much that they are being defaulted into something like a target-date fund as that the process is automatic.

Thompson says that plan sponsors should also be ready for more questions from older participants, since they pay more attention to their balances once they reach a larger amount.